If you’ve fallen behind on your mortgage payments and realize your home is worth less than what you owe the bank, you might feel like you’re “underwater” with no way out. In the 2026 Des Moines market, where home values have stabilized after years of rapid growth, some homeowners are finding themselves in this exact position.

One of the most common alternatives to foreclosure is a short sale. While the name sounds like it should be fast, the process is actually quite complex. Here is everything you need to know about navigating a short sale in Central Iowa.

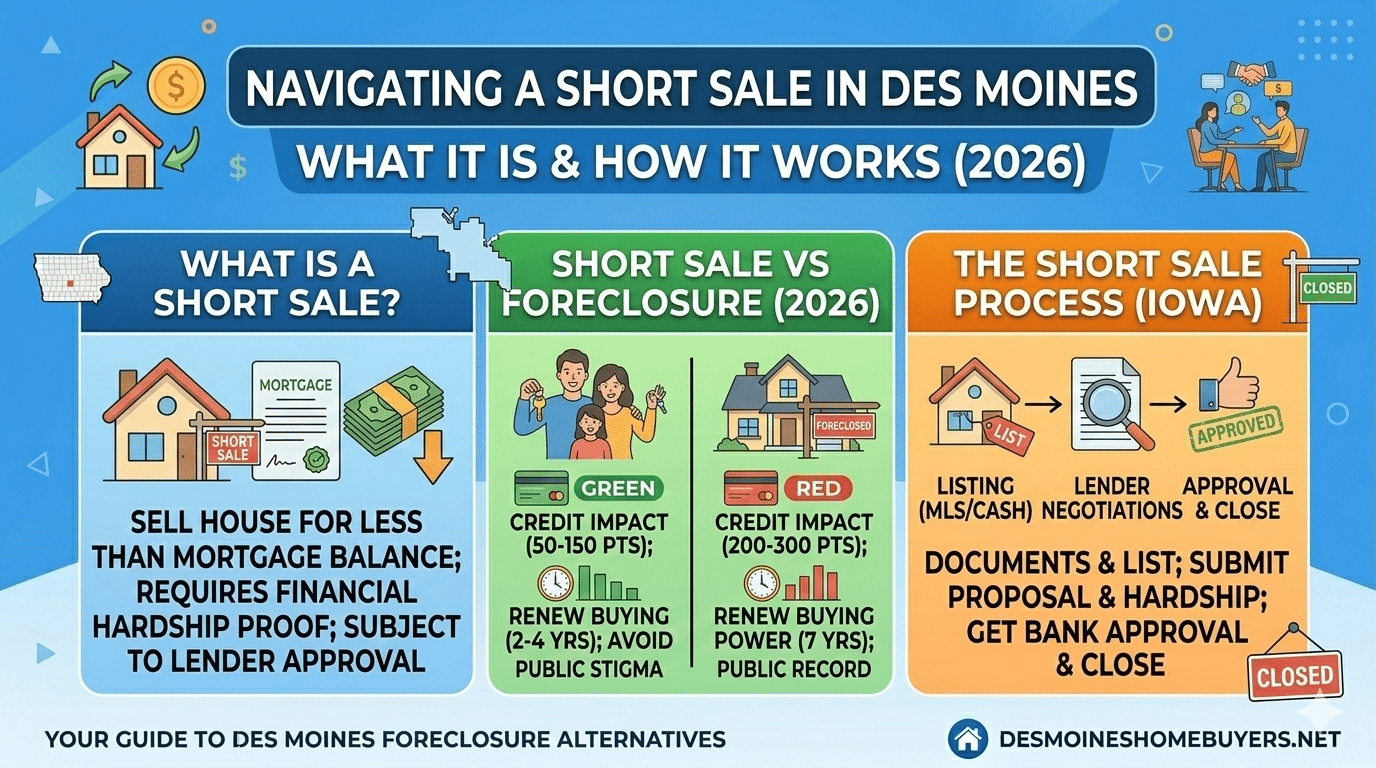

What Exactly is a Short Sale?

A short sale occurs when a lender agrees to let you sell your home for less than the remaining balance on your mortgage.

For example, if you owe $250,000 to the bank but the current market value of your home in Beaverdale or Pleasant Hill is only $220,000, you are “short” by $30,000. In a short sale, the bank agrees to accept that $220,000 as payment in full (or close to it) so the property can be sold to a new buyer.

The 3 Requirements for an Iowa Short Sale

Lenders don’t approve short sales just because you want one. In 2026, they generally require three things:

- Financial Hardship: You must prove that you can no longer afford your mortgage due to a legitimate change in circumstances, such as job loss, divorce, or medical emergency.

- A “Market” Offer: The bank won’t accept a “lowball” offer. They will conduct their own appraisal (often called a BPO, or Broker Price Opinion) to ensure the offer you’ve received is close to the home’s true 2026 value.

- Lender Approval: This is the big one. Even if you and a buyer agree on a price, the bank has the final say. If there are two mortgages on the house (like a HELOC), both lenders must agree to the deal.

Short Sale vs. Foreclosure: Which is Better?

While both result in you leaving the home, a short sale is almost always better for your financial future in Iowa.

- Credit Impact: A foreclosure can drop your credit score by 200–300 points and stay on your record for seven years. A short sale usually results in a smaller hit (roughly 50–150 points) and is often reported as “settled for less than full balance.”

- Future Buying Power: In 2026, many lenders will allow you to apply for a new mortgage just 2 to 4 years after a short sale. If you go through a foreclosure, you might have to wait up to 7 years.

- The “Deficiency Judgment”: This is critical. In Iowa, if a house is sold at a foreclosure auction for less than the debt, the bank can sometimes sue you for the difference. In a properly negotiated short sale, your attorney or agent will work to get the bank to waive the deficiency, meaning you walk away with zero debt.

The Reality: “Short” Doesn’t Mean Fast

Despite the name, short sales are notorious for being slow. Because the bank has to review your tax returns, bank statements, and hardship letter, it can take 3 to 6 months to get an approval.

In a fast-moving market like Ankeny or Waukee, many traditional buyers don’t have the patience to wait that long. This is why many short sales end up being sold to cash investors who are willing to wait out the bank’s bureaucracy.

Summary: Moving Forward

A short sale isn’t a “failure”—it’s a strategic exit. It allows you to protect your credit, avoid the public stigma of foreclosure, and start fresh sooner.

Facing a potential foreclosure in Des Moines? If you’re worried about your mortgage and don’t have the time to wait 6 months for a bank to approve a traditional short sale, we can help you look at your options. At Des Moines Home Buyers LLC | We Buy Houses for Cash Fast, we understand the Iowa foreclosure timeline and can work with you to find the best path forward—whether that’s a short sale or a direct cash purchase.

Contact Us for a Confidential Consultation and Explore Your Options Today